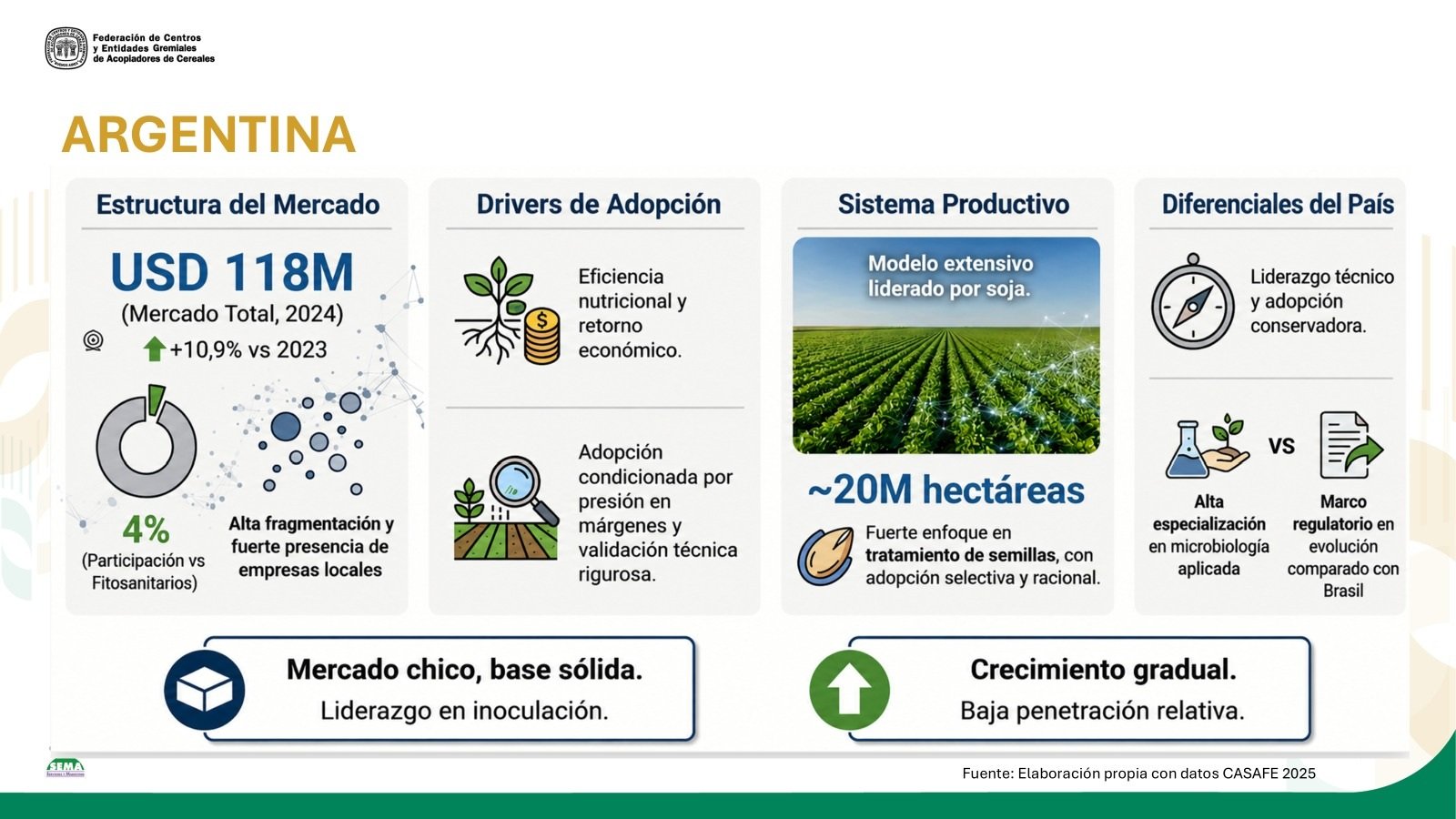

In an exclusive AgroSpectrum interview with Vinay Nair, CEO & Founder of KhetiBuddy, the discussion outlined the company’s global expansion strategy, beginning in India and North America and now extending to Europe as a natural next step driven by ecosystem readiness and structural opportunity. He emphasised that while India helped build a highly scalable, variability-driven platform for fragmented agricultural systems, Europe presents a contrasting challenge where digitisation already exists but lacks integration across farm, supply chain, and sustainability ecosystems. The interview highlighted KhetiBuddy’s differentiated approach of a standardised core platform with configurable localisation, enabling seamless adaptability across markets without compromising scalability or performance.

What structural gaps or opportunities in European agriculture made it the right next market for KhetiBuddy, and how does that differ from the Indian smallholder context you started with?

Europe is not our first international market—it is the next logical step after our expansion into North America through Canada. Our global strategy has always been driven by ecosystem readiness and the ability to solve structural agricultural challenges, not just geographic scale.

We began in India, one of the most complex agri ecosystems in the world, with fragmented landholdings, inconsistent data, and limited supply chain visibility. This forced us to build a highly scalable platform designed to operate in environments defined by variability and fragmentation, focusing on integration across farmers, input providers, financiers, and supply chains.

Europe presents a different challenge. Agriculture there is already digitised, but systems remain fragmented. Farm data, supply chains, and sustainability frameworks exist independently without meaningful integration.

Our focus in Europe is not digitisation, but integration—connecting existing systems to enable interoperability, unified visibility, and measurable outcomes across farm operations, compliance, and sustainability.

European agriculture is highly regulated and technologically advanced. How do you adapt your model without losing the scalability that defines your operations in India?

Most agritech platforms struggle to scale globally because they are built around localised assumptions—specific crop patterns, regulatory environments, or market structures—that get embedded into the core architecture. As a result, when they enter new geographies, they often require significant re-engineering or complete redesign.

Our approach is fundamentally different. We have deliberately built a standardised core platform that is consistent across markets. The underlying architecture—data models, workflows, and integration layers—remains uniform regardless of geography. What changes is not the core system, but the configuration layer on top of it.

This configuration layer allows us to adapt key variables such as agronomic practices, regulatory and compliance frameworks, language interfaces, and operational workflows to suit each market. In other words, we separate the stable technology backbone from market-specific intelligence.

Owing to this design, expansion from India to Europe is not a rebuild exercise. It is a controlled localisation process built on top of an already scalable foundation. This significantly reduces deployment complexity while ensuring consistency in platform performance.

In fact, when architecture is designed correctly, localisation becomes a strength rather than a constraint. It enhances scalability by allowing the same core system to operate effectively across diverse agricultural ecosystems without losing adaptability or relevance.

By entering Europe through a local partner, are you prioritising speed over control, and how do you mitigate risks around brand, data ownership, and execution quality?

In agriculture, entering a new market without a deep local context is one of the quickest paths to failure. The sector is shaped by regional agronomy, fragmented supply chains, entrenched relationships, and regulatory nuances that cannot be understood remotely or replicated through a purely technology-led approach.

That is why our partnership-first model is intentional. We are not exchanging control for speed; we are replacing assumptions with on-ground insight. Instead of trying to own every layer of the ecosystem ourselves, we focus on bringing a robust platform while our partners contribute critical local strengths—trust networks, farmer relationships, market access, and execution capability.

In this model, roles are clearly defined. We provide the technology backbone that standardizes data, workflows, and decision-making across markets. Our partners ensure contextual relevance by embedding the platform into existing rural and agricultural ecosystems, where relationships and credibility are essential for adoption.

From a risk and governance perspective, the structure is deliberately balanced. Data ownership remains fully with the client, ensuring transparency and control at the source. Platform governance is centralized to maintain consistency, security, and scalability across geographies. At the same time, execution is standardized through our system, ensuring that processes, outputs, and performance benchmarks remain uniform.

This means control is not diluted—it is restructured. Instead of being concentrated in one layer, it is distributed across ownership, governance, and execution in a way that preserves accountability while enabling scale and local relevance simultaneously.

How do the economics of your services translate in a higher-cost market like Europe—does profitability improve with scale, or does it depend on premium positioning?

The economics in Europe are fundamentally stronger, but that strength only translates if you are addressing the right set of problems. The nature of value creation in agriculture differs significantly between emerging and developed markets, and the monetisation model must reflect that shift.

In India, agritech economics is largely volume-driven. Value is created by reaching scale across a large base of farmers, where services are often priced for affordability and adoption. The emphasis is on breadth—serving millions of farmers through low-cost, high-frequency transactions.

In Europe, the structure is fundamentally different. The market is value-driven rather than volume-driven. Agribusinesses, cooperatives, and supply chain participants are not primarily investing in advisory services alone—they are investing in compliance, traceability, carbon accounting, and verifiable sustainability outcomes. These are not optional services; they are becoming mandatory requirements driven by regulation, ESG commitments, and global supply chain standards.

This shifts the entire business model. Instead of cost-based pricing tied to service delivery, the opportunity moves toward outcome-based pricing, where value is linked to measurable impact—such as emissions reduction, audit readiness, supply chain transparency, or sustainability certification.

In this context, scale still matters, but it plays a different role. Scale improves operating leverage and margin efficiency, but it is premium positioning and outcome credibility that determine success in the market. The ability to deliver verified, auditable, and integrated sustainability outcomes becomes the core value proposition, not just the ability to provide digital services at scale.

To what extent are your agritech solutions—developed for Indian conditions—transferable to European farms with different crop systems, climate patterns, and mechanisation levels?

Our agritech solutions were not designed specifically for India—they were designed for variability. That distinction is critical when assessing their transferability to markets like Europe.

The platform is fundamentally data-centric rather than crop-centric. This means it is not hardwired to any single agricultural system, crop type, or agronomic condition. Instead, it is built to process diverse data inputs and generate outcomes through configurable logic layers. As a result, adapting the system to a new geography does not require rebuilding the technology stack—it requires adjusting the underlying parameters, agronomic models, and regulatory rules that sit on top of it.

In that sense, Europe is not a redevelopment challenge; it is a reconfiguration exercise. The core platform remains unchanged, while inputs such as crop calendars, mechanisation practices, compliance frameworks, and sustainability standards are localised to match regional conditions.

In fact, operating in India has been the most rigorous real-world stress test for the system. We have already built and deployed across extreme variability—multiple crops, diverse climatic zones, fragmented landholdings, and inconsistent infrastructure. This forced us to design for complexity from day one.

Compared to that, Europe is structurally more standardised. Farming systems are more uniform, data quality is higher, and mechanisation is more consistent. Paradoxically, this makes deployment simpler, not harder, because the range of variability we need to account for is narrower and more predictable.

Europe’s stringent agricultural and environmental regulations can be a hurdle—do you see them as a constraint, or as a long-term competitive moat once you’re established?

In the short term, regulatory frameworks in Europe can feel restrictive, as they add layers of compliance, reporting, and validation that increase implementation complexity and time-to-market. However, over the long term, this same regulatory rigour acts as a powerful market filter that eliminates weak or non-compliant players and rewards only those with robust, transparent, and scalable systems.

We view Europe’s regulatory environment not as a constraint, but as a structural moat in the making. Regulations around carbon accounting, traceability, food safety, and sustainability reporting are becoming deeply embedded into how the agri-ecosystem operates. These are not temporary requirements—they are evolving into permanent infrastructure for how agricultural value chains are governed and evaluated.

Once a platform is fully aligned with these frameworks, its role shifts significantly. It is no longer just an external service provider; it becomes embedded within the compliance and reporting architecture of the ecosystem itself. Whether it is carbon measurement, supply chain traceability, or sustainability disclosures, the platform becomes a trusted layer through which data is generated, validated, and reported.

This creates a much stronger form of defensibility. Instead of competing on features or pricing alone, the value shifts to system integration and regulatory alignment. At that point, switching costs increase significantly, and the platform becomes difficult to replace without disrupting compliance workflows and reporting continuity.

In this sense, regulation does not just shape the market—it defines the entry barrier and ultimately determines who becomes structurally embedded in the ecosystem versus who remains peripheral.

Unlike India, Europe already has a dense ecosystem of agritech players—what is the core differentiation that allows you to compete against well-funded incumbents?

Yes, Europe already has a large and mature agritech ecosystem, with many companies addressing specific parts of the agricultural value chain. However, most of these solutions are built to solve narrow, well-defined problems in isolation—farm management, traceability, precision agriculture, or sustainability reporting as separate use cases.

The limitation is not the absence of technology; it is the fragmentation of it. Different systems operate independently, creating data silos across farm operations, supply chains, compliance frameworks, and sustainability reporting. As a result, agribusinesses often end up managing multiple platforms that do not communicate effectively with each other.

Our approach is focused on solving this structural gap. Instead of competing as another point solution, we are building the connective layer that brings these fragmented systems together into a unified data backbone for agribusinesses. The objective is to enable interoperability across existing platforms rather than replace them.

This means we sit above individual tools and systems, integrating data flows across farm operations, traceability systems, sustainability frameworks, and regulatory reporting structures. In doing so, we enable a single, consistent view of agricultural activity across the entire value chain.

That is the fundamental distinction. We are not positioning ourselves as another standalone application in an already crowded landscape. We are building the underlying layer that allows all these systems to function together coherently, turning fragmented data into a connected, usable, and decision-ready ecosystem.

As you expand internationally, how do you balance global growth ambitions with your original mission of supporting farmers at the grassroots level—does scale risk diluting impact?

Our mission has not changed in its intent—it has evolved in its scope and the level at which we intervene. We began at the farm level because that is where the challenges in agriculture are most immediate and visible—uncertain incomes, fragmented inputs, limited market access, and lack of reliable advisory. Working directly with farmers allowed us to understand ground realities in depth and build solutions rooted in real constraints rather than assumptions.

However, over time, it became clear that sustainable, large-scale impact cannot be achieved by addressing farms in isolation. Agriculture is a systems-driven sector, where outcomes at the farm level are heavily influenced by decisions made upstream and downstream—by agribusinesses, supply chains, financial institutions, and policy frameworks.

Owing to this, the real leverage lies not in optimising individual farms one by one, but in enabling the platforms and institutions that collectively influence thousands or even millions of farms at once. This includes improving how agribusinesses manage sourcing and distribution, how supply chains ensure traceability and efficiency, and how policymakers design and monitor agricultural interventions.

This shift does not represent a departure from impact—it represents an evolution in how impact is created. Instead of limiting ourselves to direct, localised interventions, we are scaling our influence through system-level enablers that multiply outcomes across the ecosystem.

In that sense, the work becomes more structural and far-reaching. We are not moving away from farmers or impact at the ground level; we are extending that impact by shaping the systems that determine farmer outcomes at scale.

-- Suchetana Choudhury (suchetana.choudhuri@agrospectrumindia.com)