“The current escalation in the Middle East is hitting commodity markets hard. Whether the conflict becomes deadlocked will determine the extent of the current shock on the downstream part of the value chain,” says Simon Lacoume, sector economist at Coface.

25 days after the launch of the Israeli American offensive against Iran, disruptions to the supply of raw materials via the Strait of Hormuz continue to fuel prices volatility. For the time being, oil & gas, fertilizers, petrochemical derivatives and aluminum are particularly affected.

“The current escalation in the Middle East is hitting commodity markets hard. Whether the conflict becomes deadlocked will determine the extent of the current shock on the downstream part of the value chain,” Simon Lacoume, sector economist at Coface.

Oil prices: a long-lasting shock

The recent attacks on the Ras Laffan gas complex in Qatar have triggered a further rise in the price of energy commodities. Brent crude, peaking at $119 last week – rose by 50% in a month. This rise is not uniform. Oman DME crude has exceeded $160 per barrel, whilst US WTI is hovering around $100 per barrel, reflecting a highly uneven impact on prices depending on the region and the product. As the conflict drags on, this rise is already beginning to spread down the value chain. In the United States, regular gasoline retail prices have reached an historic high ($3.96/gallon, up 35% month-on-month). In Asia, diesel prices (Singapore) have almost tripled since the start of the conflict, to $256/barrel, whilst global jetfuel prices have doubled, according to the International Air Transport Association (IATA).

Natural gas at the heart of supply disruptions

The rise is also evident in natural gas. In Europe, gas futures contracts (the Dutch TTF index) have surged by 85% in a month, to €55/MWh, whilst the Asian benchmark (LNG Japan/Korea Marker) has doubled over the same period, reflecting the persistent vulnerability of importing markets. By comparison, the US market appears less exposed to supply disruptions. The US Henry Hub is nonetheless under strong upward pressure (+36% month-on-month), a sign that energy tensions have already spread globally.

Prices for many petrochemical compounds are rising exponentially

The Gulf states are Asia’s leading suppliers of petrochemical products1 , which are essential to the entire plastics industry. A ton of naphtha has reached $1,000 in Singapore, an increase of over 60% since the start of the conflict. The combination of tensions in the Strait of Hormuz and historically low Asian stocks (2 to 3 weeks) has already driven up the prices of polymers (polypropylene, polyethylene, polystyrene, PVC). This now poses a risk of spillover across the entire value chain. Consequently, this trend is also affecting sulfur, a key input for the leaching2 of copper and nickel ore. The 25% price rise in a single month is putting major, highly dependent mining producers such as Chile, the Democratic Republic of the Congo and Indonesia at risk.

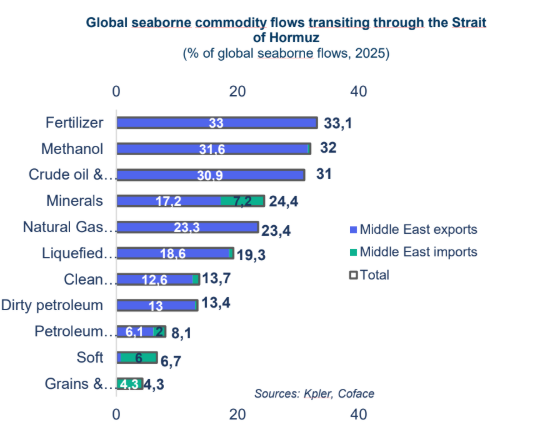

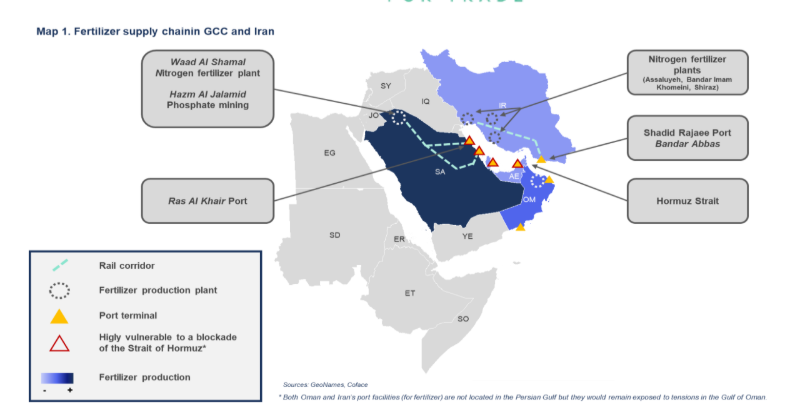

Fertilizer prices are soaring, despite a ‘favorable’ agricultural calendar

Thanks to cheap domestic energy supplies, the Gulf states3 occupy a central position in these markets, accounting for nearly 19 % of global nitrogen fertilizer exports and 36 % of global urea volume, whilst Saudi Arabia is the 4th largest exporter of phosphates (Map 1). However, natural gas accounts for up to 80% of nitrogen fertilizer production costs. The surge in gas prices therefore automatically leads to a rise in fertilizer prices: the price of a ton of granular urea (FOB Middle East) has risen by 37%, to $665, since the start of the conflict. The impact remains limited, however, given a favorable timing. For the moment, only US grain producers appear to be affected, but if the disruptions were to persist, then Brazil, India or even Europe would be more exposed.

The negative effects could even extend beyond direct fertilizer flows – to India, Brazil or the United States, for which the Gulf states account for 63%, 24% and 21% of nitrogen fertilizer imports respectively – by affecting third countries such as Morocco, the world’s leading producer of phosphate rock, which is heavily dependent on sulfur exported by the Gulf states.